Could Poor Supplier Carbon Data Increase Your Cost of Debt?

Published:

Read Time: 5 mins

Why Scope 3 emissions are moving from the sustainability report to the lender's risk model

By Graham Paul, Service Delivery Director, TEAM Energy

For years, Scope 3 emissions have been viewed as the most challenging part of corporate sustainability reporting. They are difficult to measure, complex to manage and often sit outside an organisation's direct control

As a result, many organisations still treat Scope 3 reporting as a compliance exercise, one that needs improving over time, rather than a priority today.

That mindset may be about to change

A growing number of lenders are incorporating ESG performance into lending decisions, and supply chain emissions data is becoming part of the conversation. What was once a sustainability reporting challenge is rapidly evolving into a financing issue. Organisations that lack visibility of their Scope 3 emissions may find themselves facing more difficult discussions with investors, lenders and procurement teams in the years ahead.

The emissions challenge hiding in plain sight

Most organisations are surprised when they calculate their first comprehensive Scope 3 footprint.

According to the Carbon Trust, Scope 3 emissions often account for between 70% and 90% of an organisation's total carbon footprint. Research from CDP and Boston Consulting Group found that supply chain emissions are, on average, 26 times greater than combined Scope 1 and Scope 2 emissions. Yet only a relatively small proportion of organisations have set formal Scope 3 reduction targets.

For many businesses, the largest environmental impact does not come from their own buildings, vehicles or energy consumption. It comes from purchased goods and services, outsourced operations, logistics networks and supplier activities.

This means that the quality of an organisation's sustainability reporting increasingly depends on the quality of information it receives from suppliers.

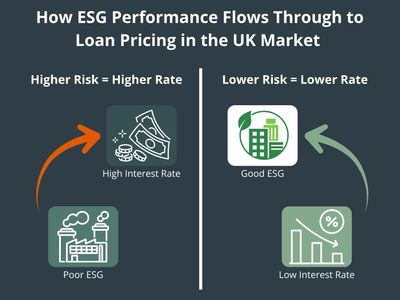

Why lenders care about Scope 3

Historically, lenders focused almost exclusively on financial performance when assessing risk. Today, many are taking a broader view.

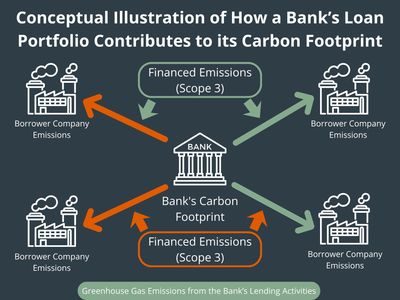

With evolving sustainability reporting requirements, financial institutions are finding themselves under pressure to understand the climate-related risks within their portfolios. This includes the emissions associated with the organisations they lend to.

More often, banks and investors are being asked to account for financed emissions. To meet their own sustainability reporting obligations, they require credible information from borrowers on both direct operational emissions and material supply chain impacts. Under the GHG Protocol, financed emissions reporting can include emissions associated with lending portfolios, making access to robust borrower data more important.

Recent research suggests that 73% of UK mid-market lenders now have a formal ESG lending strategy, while 81% expect ESG performance to play a more important role in lending decisions over the next five years.

In other words, sustainability information is no longer sitting on the periphery of financial decision-making. It is moving closer to the centre.

The emergence of the "carbon credibility" test

The most interesting shift is not whether organisations can produce a carbon footprint.

It is whether they can stand behind the quality of the data used to calculate it.

Lenders, investors and procurement teams are becoming more sophisticated in their assessment of ESG claims and want to understand how emissions figures have been calculated whether supplier data has been verified and what governance structures support reporting processes.

Two organisations may publish nearly identical carbon footprints, yet one is underpinned by verified supplier data, active engagement programmes and a clear decarbonisation strategy, while the other relies heavily on broad estimates. As ESG expectations mature, stakeholders are looking beyond the headline numbers. The focus is shifting from the emissions figure itself to the quality and credibility of the data behind it. Organisations with transparent methodologies, robust governance and a clear roadmap for improving data quality are likely to earn greater trust from lenders, investors and customers alike.

A business borrowing issue

This is where the conversation becomes particularly relevant for boards, finance directors and business owners.

Many organisations still view ESG as the responsibility of the sustainability team. In reality, some of the most significant implications sit within finance, procurement and risk management.

There is growing evidence that sustainability performance can influence access to capital. Sustainability-linked lending products already link financing terms to environmental performance targets, while some lenders are introducing preferential terms for qualifying sustainability initiatives. Conversely, weaker ESG performance can create the perception of increased business risk.

Whether businesses face an explicit pricing adjustment today is less important than recognising the direction of travel.

As climate-related financial risks become more embedded in lending frameworks, organisations with stronger data, clearer governance and credible transition plans are likely to be in a stronger position during funding discussions.

Credibility is more important than perfection

The good news is that businesses do not need perfect data from every supplier before taking action.

In fact, attempting to achieve complete precision from day one is often one of the biggest barriers to progress.

Leading organisations typically start by identifying emissions hotspots, prioritising high-impact suppliers and improving data quality incrementally. Over time, they move from broad estimates towards more detailed supplier-specific information, focusing effort where it delivers the greatest value.

The goal is not perfection. It is credibility.

Businesses that can demonstrate an understanding of their supply chain emissions, active supplier engagement and a clear plan for improvement are likely to be viewed more favourably than those waiting for perfect information before they begin.

Looking ahead

The next phase of corporate sustainability reporting will be defined by value-chain transparency.

Scope 3 emissions are no longer simply a reporting metric for sustainability practitioners. They are becoming an indicator of organisational resilience, governance maturity and strategic risk management.

For organisations seeking growth, investment or external finance, the question may soon extend beyond "What are your emissions?"

Instead, the question may become: "How confident are you in the data behind them?"

Those that can answer that question with confidence may discover that effective sustainability reporting does more than satisfy ESG requirements, it helps strengthen business resilience, stakeholder trust and financial credibility.

Ends

Editors notes

About TEAM

TEAM is an energy and sustainability consultancy. It helps organisations with large energy estates reduce consumption and carbon emissions to save money and meet commercial and compliance targets on their journey to net zero.

Founded in 1985, it has a long history of helping customers navigate changing definitions and certification standards. TEAM Energy is an Employee Ownership Trust (EOT), with employees having a direct stake in its customers’ success.

Graham Paul is Service Delivery Director at TEAM Energy, helping organisations develop robust energy, carbon and sustainability reporting strategies. He works with public and private sector organisations to improve data quality, strengthen ESG reporting and support the transition to net zero.